In its most recent statement the FOMC stated “Inflation is anticipated to remain near its recent low level in the near term, but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of earlier declines in energy and import prices dissipate. The Committee continues to monitor inflation developments closely. ” We decided to put together a monitor to extract the main components of inflation to track the dynamics in the core factors. To do so we have chosen to group the major Inflation measures into four categories, Consumer, Producer, Wages, and Expectations. Each category contains below time series:

For each category we use year-over-year data with the exception of ISM manufacturing and non-manufacturing diffusion indices which we keep as levels. We then standardize each series by subtracting the mean and dividing by the series’ standard deviation. We then extract the first principal component and also normalize it in a similar fashion to take out the z-score.

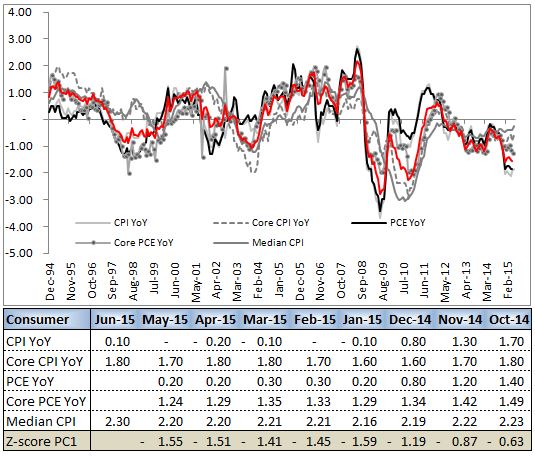

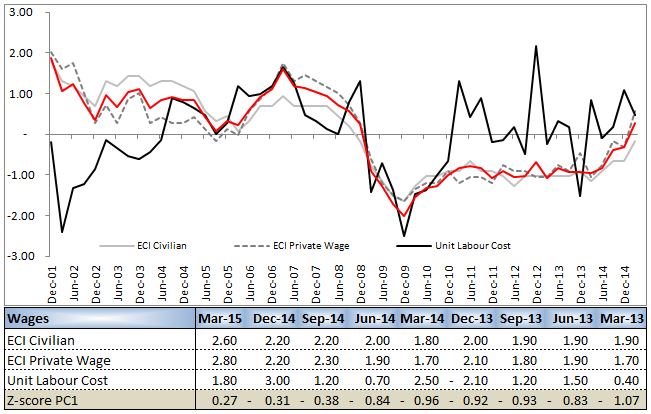

The first principal component captures 67% of the variation in the Consumer batch of series, 72% of the variation of the Producer batch, 65% of Wages and 82% of the Expectations.

The results are presented below. The consumers data is running well below its historical average. The z-score of the first principal component is -1.55.

Similarly, the z-score of the first principal component for the Producer series. With the exception of PPI Finished Goods excluding food and energy all other series are well below their historical average.

There appears to be no inflation pressure at either at the consumer or the producer level. As noted by the FOMC wages have been improving recently and this fact is well captured by the first principal component that we have extracted from the aforementioned time series.

The trend is higher in all three time series along with our extracted principal component. Interestingly this trend is not feeding into the other measures and indicates possible pressures on corporate margins with labour costs increasing while rest of prices still running below their historical averages.

Finally, when we look at different measures of inflation expectations and extract the main component we again see a pickup of the levels but still running below historical average.

To get a better visual representation of each series we present a heatmap of the historical z-score for each category and also a combined simple average. It is very clear that there is hardly any inflation pressure in the system and therefore any catalyst for a rate hike will be driven by dynamics in the labour market rather than the inflation side of the Fed’s dual mandate.

These results corroborate our suspicion that current break evens are too high despite coming off recently. A simple model with PMI, Comdty price index and Fed expectations (along with intercept correction for the credit crisis which distorted prices due to liquidity issues) reveals that current 10yr breakeven inflation is trading too high.

This simple model has a much better fit than more complicated models which include typical economic factors such as CPI, CPI vol, money growth, gasoline prices and other macro variables.